Already in our 2016 energy forecasts, we foresaw a much more favourable development of renewable energy than authoritative organizations: energy companies, the oil industry and international bodies like the IEA. Finally, from 2021 onwards, they start revising upwards their forecasts. But they also predict an ongoing growth in global energy consumption. Whereas we foresaw (and foresee) stabilization.

Since 2016, global energy consumption rose by a mere 4%; or a meagre 0.6% annually. Per capita, global energy consumption is just a little bit above 0%. Do we, in our energy forecasts, foresee a decline in energy use per capita of the world? Will we speed up further in sustainable energy growth? Will energy become dirt cheap again in the long run? We keep up our spirits, but a lot of work needs to be done. Sustainable energy mainly delivers electricity; and that is just 15 to 20% of total energy production. Can we multiply that by five, in order to become entirely fossil free?

Since 2016, global energy consumption rose by a mere 4%; or a meagre 0.6% annually. Per capita, global energy consumption is just a little bit above 0%. Do we, in our energy forecasts, foresee a decline in energy use per capita of the world? Will we speed up further in sustainable energy growth? Will energy become dirt cheap again in the long run? We keep up our spirits, but a lot of work needs to be done. Sustainable energy mainly delivers electricity; and that is just 15 to 20% of total energy production. Can we multiply that by five, in order to become entirely fossil free?

The incumbents’ energy forecasts

Up to ca. 2020, major players in the energy world forecasted continued energy growth. In 2016, BP forecasts a total of 18,000 mtoe in 2035, up from 12,500. So far, we didn’t even hit 14,000. Shell foresees 22,000 in 2040 and 25,000 in 2050 (double the 2016 amount). In its Sky scenario energy forecasts, Shell expects a 50% growth; with a continued important part played by fossil energy (ca. 50/50 in 2050). This implies a major carbon capture and storage effort. In reality, we see very little coming in this field. At times there are science fiction-like stories about CO2 capture from ambient air; and stories about chemists who promise to make any molecule from CO2. A matter of daydreaming, actually. Carbon capture and storage will cost money. Whatever the scheme, the tax payer will have to pay for this. It is challenging to look upon CO2 as a resource for chemical industry (materials, medicines, molecules), but this won’t get us anywhere in the energy transition. The chemical sector is just 5% of the energy sector.

In the IEA energy forecasts, there is just one scenario that results in stabilization; the so-called IEA450 picture, where 450 is shorthand for the upper limit of ambient CO2 (in ppm). The IEA doesn’t believe that it can become a reality; and the scenario tends to be the result of what it would take to keep CO2 below 450 ppm. For renewable energy, the incumbents predict a cumbersome start. It will peak at about 20%, so they figure. The IEA figures on solar energy tell the whole tale. Each year they need to revise their estimates upwards; they cannot deny reality. But then anew, they predict almost zero growth. The IEA World Energy Outlook also shows this pessimism.

Reality in year 2023

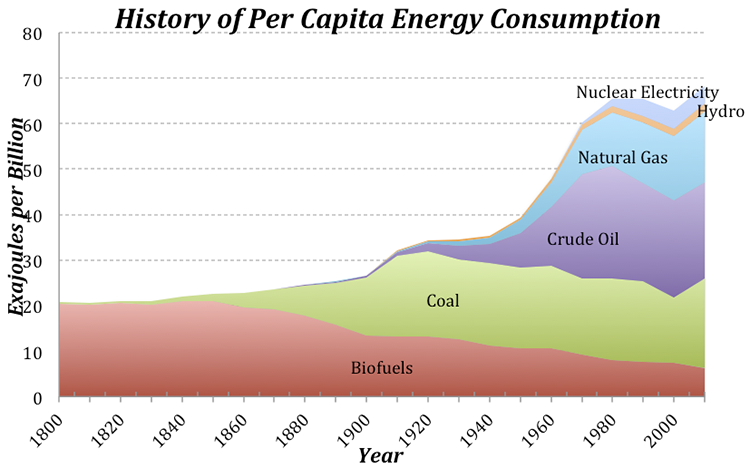

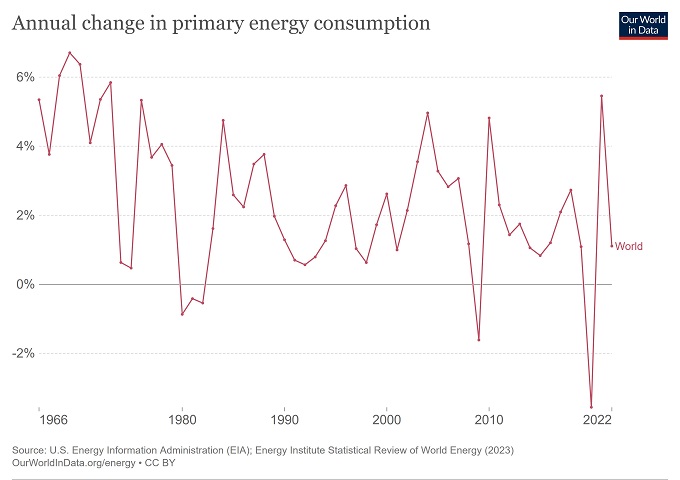

Figures can just show the past. For energy forecasts, we should rather have a look at trends. The breakthrough of solar and wind energies is obvious. The growth percentages are far beyond all expectations, and far beyond business-as-usual. Their growth is just stunning. Pessimists and incumbents will now quickly tell us that we will not be able to sustain such a growth. But solar and wind keep on growing, and at an accelerating pace! Nobody looked at global energy consumption per capita. This hardly grows anymore. For more than 10 years already, the figure hovers about 75 GJ per capita per annum. The result of all calls for energy conservation? Some call energy conservation is called the cheapest sustainable energy source. It could be, but it is more likely that the market reacts on expensive energy.

Energy equipment and energy applications tend to conserve more and more energy. All appliances now have an energy label – and less is better. We haven’t yet reached the end of this development by far. Take for instance the Amsterdam internet data centre; because of new equipment, it now functions on 85% less energy. In this area, we are still picking ‘low hanging fruit’. In the domestic realm, energy labels just start having an effect on real estate prices. We just started to conserve energy; industry just started to produce energy conserving equipment. We already wrote about these processes in our publications More with Less, Biobased Press 2017, and De oplossingen zijn er al (in Dutch), Biobased Press 2020.

The near future

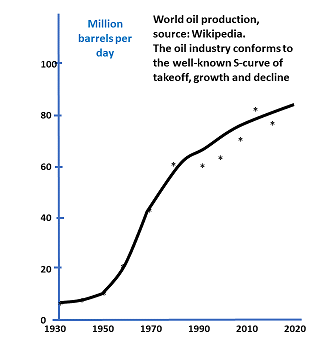

In terms of the well-known S-curve for major industrial and economic developments, we find the oil industry in the phase of consolidation and decline; whereas renewable energy moves around the turning point from an embryonic start to exponential growth. The point where fossil industry was in 1950. According to the well-known think tank RethinkX, a development needs violent events in order to take it into the phase of exponential growth. For the oil industry, that was WOII, and the major surge in energy demand as the world was rebuilt after the war.

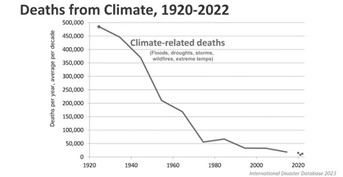

For the development of renewable energy, the Russian-Ukrainian war is a first event of the required impact. Moreover, the present violent climatic extremes will amplify the call for renewable energy. But some will deny this, and draw attention to the figures published very recently on victims of violent climatic events (see figure and this link). Our perspective is entirely different; didn’t we just witness climate change at work in the floods in Slovenia? And as the figure shows, the trend is almost horizontal from 1970 onwards. We can safely predict from this graph a growth in victims of natural disasters. That is how we feel; and that will have its effect on anything developed and offered to us, with the purpose to stay safe from danger.

For the development of renewable energy, the Russian-Ukrainian war is a first event of the required impact. Moreover, the present violent climatic extremes will amplify the call for renewable energy. But some will deny this, and draw attention to the figures published very recently on victims of violent climatic events (see figure and this link). Our perspective is entirely different; didn’t we just witness climate change at work in the floods in Slovenia? And as the figure shows, the trend is almost horizontal from 1970 onwards. We can safely predict from this graph a growth in victims of natural disasters. That is how we feel; and that will have its effect on anything developed and offered to us, with the purpose to stay safe from danger.

Where are the bottlenecks?

No doubt, very many publications, books, social media, talk shows and the like will tell us that 100% renewables is an impossibility. As always, it is simpler to predict that something is impossible than the other way around. For the simple reason that most of the time, the general public is worse in energy forecasts than the expert. Let’s have a look at a number of factors that will facilitate the transition.

Firstly, we have to answer the question if we need 100% renewables. Somewhere around 50% might do as well. As long as the trend of increasing CO2 concentrations in the atmosphere would be reversed to a decrease. Preferably before 2030. Quite possible, if energy demand stabilizes, as is the case now, whereas solar and wind energies will take an increasing share of that amount.

Developments

But more developments have started with an effect on energy forecasts in the 5 years to come:

- There will be increasing attention from policy for energy intensive sectors like the steel and cement industries. And we know by now that there are alternatives to them.

- The trend towards low-energetic equipment and applications has just started. Led lamps and home insulation make for a good start. New building regulations, energy storage and heat pumps will herald a new phase in this development.

- The chemical and material sectors are not yet half-way in the realisation of their proposed plans to become more sustainable and more energy efficient.

- So far, reuse requires more energy than direct production, using fossil fuels. In the course of time, we will see this changing. Moreover, we will become smarter in reuse, using solar and wind energy exclusively. And then there is no need any more to be energy efficient.

- Last year, mankind installed 1,200 solar panels per minute; 10 years ago, this number was 100. This year, we will hit the 2,000 mark. Developments in China go fastest, but the Netherlands and Australia head the race if we judge by the number of panels per capita (more than 1 kW per capita). There is a lot of room, still many uncovered rooftops. And then, there are parking lots and highways that we can very well cover with solar panels. And charging while driving or being parked.

- At sea, we can construct solar panels in between wind turbines. Shipping is forbidden anyway in those locations, and the infrastructure to transport electricity is in place already.

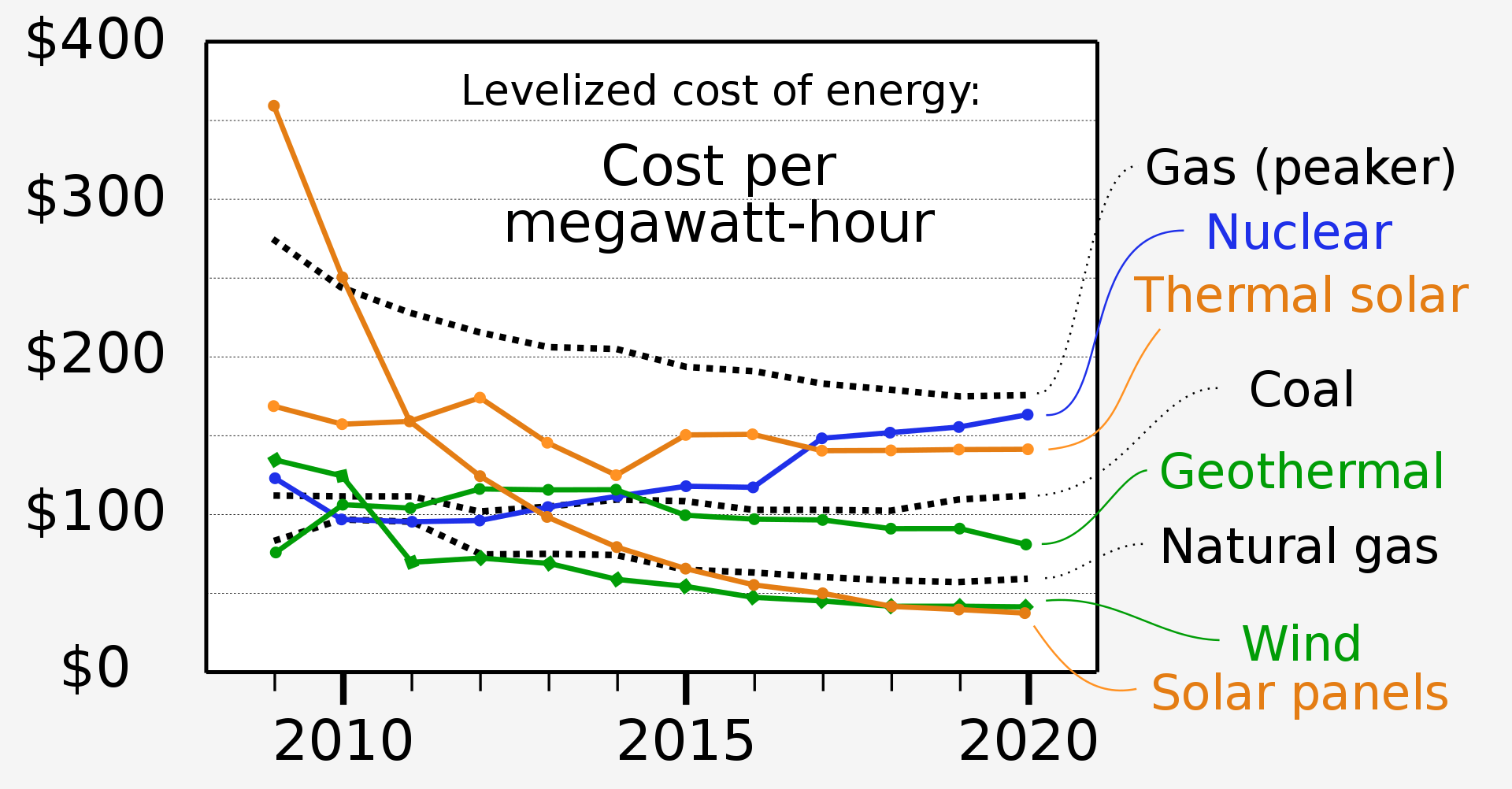

- Several years ago, we installed solar panels with a yield of about 15%. Not because that was as high as we could get, but because we could produce such panels in large numbers. Now, our choices are much larger. Panels with a yield of 30% are on the verge of market introduction.

- Installing panels becomes easier all the time; and integration in and around the house becomes much more versatile.

- Both for home owners and entrepreneurs, becoming energy self-sufficient is getting ever more attractive. Not just in terms of energy production now, but in the near future also in storing energy. Storing energy in motor car batteries is just a start. Our electricity companies can make much better use of this opportunity, and in doing so, relieve themselves of the duty to install spare capacity.

- There are still major opportunities for wind energy. In the Netherlands, our perception is dominated by the situation in our densely populated country. Elsewhere, and at sea, there are many opportunities. The number of major wind energy projects worldwide increases all the time, both on-shore and off-shore. Installation in the North Sea has been very successful, so far.

- People will tell us again and again that shortage of essential materials is looming; and that discarded panels and wind turbines are a problem. They will tell us panicky stories about shortages in steel and cement, gallium, germanium, cobalt, lithium – not to mention those rare earth metals with their difficult names. These are problems that will play a role at a certain moment, but for which solutions are either present or underway. We will have to learn to make the correct choices at the right moment.

Hydrogen and energy storage

Will the optimism of the preceding paragraphs carry us the energy forecasts required by the looming climate problem? No. Solar, wind and water energy only produce electricity. By far not even half of global energy consumption. Electricity now accounts for just 15-20% of it. Maybe this can grow to 50%. And then we include nuclear energy, that also produces electricity.

So, we don’t have an electricity problem. We have ample opportunities to produce it. Even though production and consumption will not always match easily. Storage and transport of electricity are not as easy by far as those of oil, coal and gas. But here, we refer to the title of our latest book (in Dutch): ‘The solutions already exist!’ Take for instance the Middle East and the countries in the Northern part of Africa. These countries can lose the globally dominant position they have in the fossil industry; but they also have the resources and the space to produce electricity at a giga scale from solar, wind and nuclear, for just a few cents per kWh. Literature shows that countries like Morocco and Saudi Arabia have mega plans for the production of electricity, and from there to hydrogen, ammonia and other energy carriers. Other countries with comparable geographic conditions will certainly follow; or they are active already. Like Western China, Australia, the USA; and ultimately thinly populated countries like Kazakhstan, Argentina, Russia, parts of Pakistan and India, Iran, Iraq, Northern Africa and (hopefully) the Sahel.

New perspectives

Therefore, in the longer run, say 25 years, we will see completely new global energy forecasts coming. Because all countries have access to sun, wind and water, almost all countries will be able to fulfil their energy needs for at least some tens of percent. They will be able to top that if they would have access to storage in large batteries (a development of which we witness just the start). Storage in the form of hydrogen (or ammonia, or comparable energy carriers easily produced by cheap electricity) will take them a step further towards energy independence. And yet, geopolitical tensions will not disappear completely. Countries well positioned to produce electricity at very low cost, will of course use that position for the production of competing energy carriers. To be transported to population centres through long-distance high voltage lines, or through hydrogen, ammonia, heat or whatever else.

But changes on the scale envisaged, based on new technologies, cannot succeed without new policies. Is the world ready to accept them? We should start new educational courses, intended for workers to acquire the right skills. Ensure that new employment starts at the local scale. Take measures to ensure that solar industry doesn’t stay concentrated in one country (China), but make sure that each continent has an industry of its own. Develop policies that support this, like technology development, adequate regulation, and political and public support. Make sure that technical standards and quality control are adequate. Industry should be supported by financial stimuli; renewable energy should be able to attract capital. Industry should deploy economies of scale and good business models. As technical impediments have been conquered to a large extent, we should pay attention to these issues.

In short

Our energy forecasts show that the world will be much different in a few decades’ time. Many countries will want to produce the majority of their energy (i.e., electricity) within their own borders. Solar, wind and water offer ample opportunities in that area. The energy they will produce will be sufficiently cheap. In addition to that, the world will need liquid energy carriers. Substances that can be very well produced in countries well-endowed with solar irradiation. We will transport energy carriers around the world; no oil anymore but intermediaries like hydrogen or ammonia. Through pipelines or by ship. For the next decade, we will still witness confrontations between different energy prospects. But then the battle will subside. Renewable energy will have won. There is a new world energy order coming. Energy will much less constitute a source of international tension.

Interesting? Then also read:

Green energy transition will be cheap

Solar and wind energy: increasing recognition

Energy storage will accelerate the transition